Measurements in Financial Reporting: Assets and Liabilities

In financial reporting, understanding the measurements of assets and liabilities is crucial for accurately depicting a company’s financial health. This involves categorizing assets and liabilities into current and non-current groups, providing stakeholders with detailed insights into the company’s short-term and long-term financial obligations. These precise measurements in financial reporting ensure compliance with accounting standards and facilitate strategic decision-making.

Join over 2 million professionals who advanced their finance careers with 365. Learn from instructors who have worked at Morgan Stanley, HSBC, PwC, and Coca-Cola and master accounting, financial analysis, investment banking, financial modeling, and more.

Start for Free

Understanding how to measure assets and liabilities is vital for depicting a company’s financial health accurately. Assets and liabilities—the fundamental elements of a balance sheet—are categorized into current and non-current groups to provide clear insights into a company’s financial state.

This categorization aids stakeholders in assessing the company’s short-term solvencies and long-term obligations. Measuring these elements accurately—a key aspect of measurements in financial reporting—is essential for effective financial management and strategic decision-making—reflecting Peter Drucker’s assertion that “If you can’t measure it, you can’t manage it.” Through this approach, companies ensure compliance with accounting standards and offer transparent reporting to their stakeholders.

Assessing Financial Statements

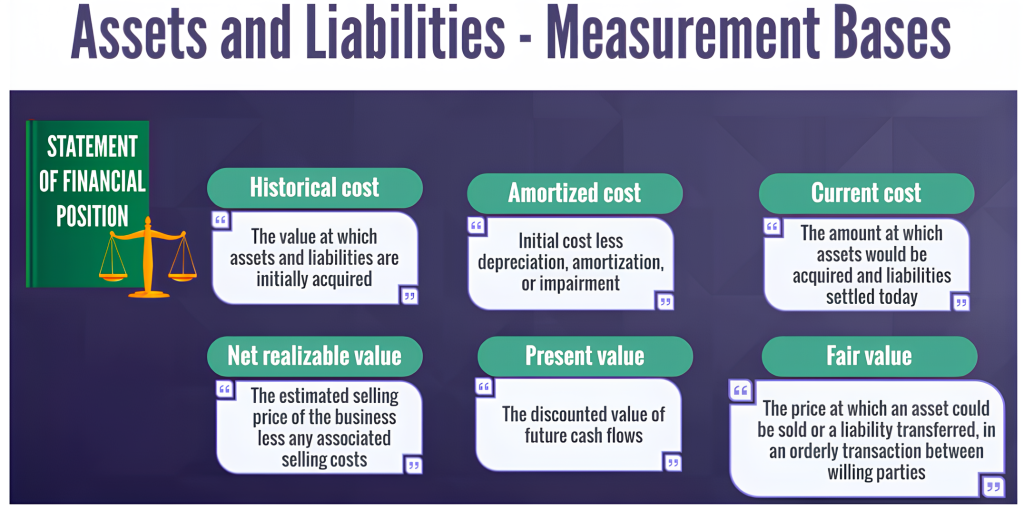

Overview of Measurement Bases

Companies use diverse measurement bases in financial reporting, including historical cost, amortized cost, and fair value.

Balance Sheet Measurements

Assets on balance sheets are often valued initially at cost, such as cash, prepayments, and accruals. Standards like International Accounting Standard 2 (IAS 2) dictate that items like inventory should be recorded at the lower historical cost or net realizable value (NRV). For example, a solar panel manufacturer may have inventory costing $105 million, but if the NRV after selling costs is only $100 million, this lower figure is used in the financial statements.

Accounts Receivable

Under International Financial Reporting Standard 9 (IFRS 9), Accounts Receivable is classified as a financial asset and reported at NRV—a critical component of measurements in financial reporting. NRV is the total receivables minus any allowance for doubtful accounts—representing the estimated uncollectible amounts. For example, if a company has $50,000 in total receivables and anticipates $10,000 as bad debt, the NRV would be $40,000.

Property, Plant, and Equipment (PPE)

Cost Model

IFRS and US GAAP mandate reporting property, plant, and equipment (PPE) at amortized cost—initially recorded at historical cost less accumulated depreciation. For instance, a $5,000 machine with $1,500 accumulated depreciation has an amortized cost of $3,500. An exception is land, which is not depreciated and maintains its value indefinitely.

Revaluation Model

Alternatively, IFRS allows the revaluation model, reporting PPE at fair value less accumulated depreciation. Changes in fair value are recorded in equity under the revaluation surplus. This model reflects the current market value of assets.

Investment Property

Investment property can be reported at cost or fair value, with changes in fair value recognized in the income statement rather than equity.

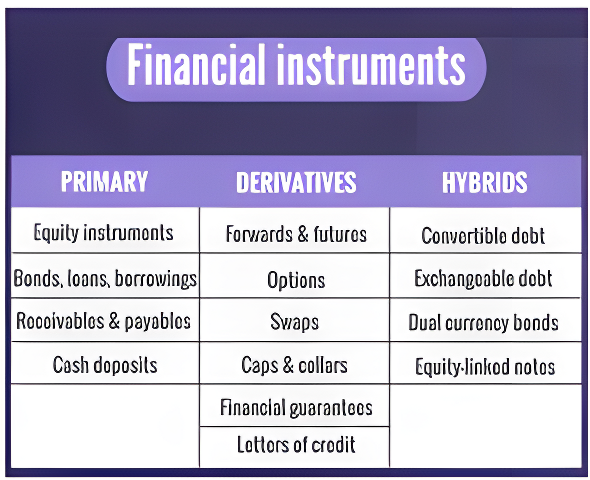

Financial Instruments

Financial instruments—including primary instruments like equity and fixed-income securities and derivatives like forwards and futures—can be assets and liabilities. They’re measured at historical cost, amortized cost, or fair value based on specific reporting standards guidance—pivotal aspects of measurements in financial reporting. Understanding their measurement can be complex due to the dual nature of these instruments.

Reporting standards provide clear guidance on the treatment of a broad range of instruments—typically measured at historical cost, amortized cost, or fair value. While many instruments are not covered here, those that are can be measured either at cost or fair value. Under the fair value method, assets are categorized into two main groups, with fair value changes reported either in the income statement or the Statement of Comprehensive Income (SCI)

Ensuring Transparency & Accurate Measurements in Financial Reporting

The measurement of assets and liabilities—a fundamental aspect of measurements in financial reporting—is crucial for accurate financial reporting. Standards like IFRS and US GAAP provide comprehensive guidelines that ensure the clarity and reliability of financial statements. Companies can accurately reflect their financial status by categorizing assets and liabilities and employing measurement bases like historical cost, amortized cost, or fair value. This meticulous approach enhances transparency, aids in compliance with regulatory standards, and builds stakeholder confidence in the company’s financial health.

To further deepen your understanding of financial reporting and enhance your professional skills, consider joining 365 Financial Analyst—a platform designed to equip you with the knowledge and tools needed for success in the financial sector.