Advanced Machine Learning and AI Applications in Finance

This course explores recent developments in machine learning and AI applied to financial time series, portfolio optimisation, and asset pricing.

Start for free

Start for free

What you get:

- 3 hours of content

- 2 Interactive exercises

- 8 Coding exercises

- 46 Downloadable resources

- World-class instructor

- Closed captions

- Q&A support

- Future course updates

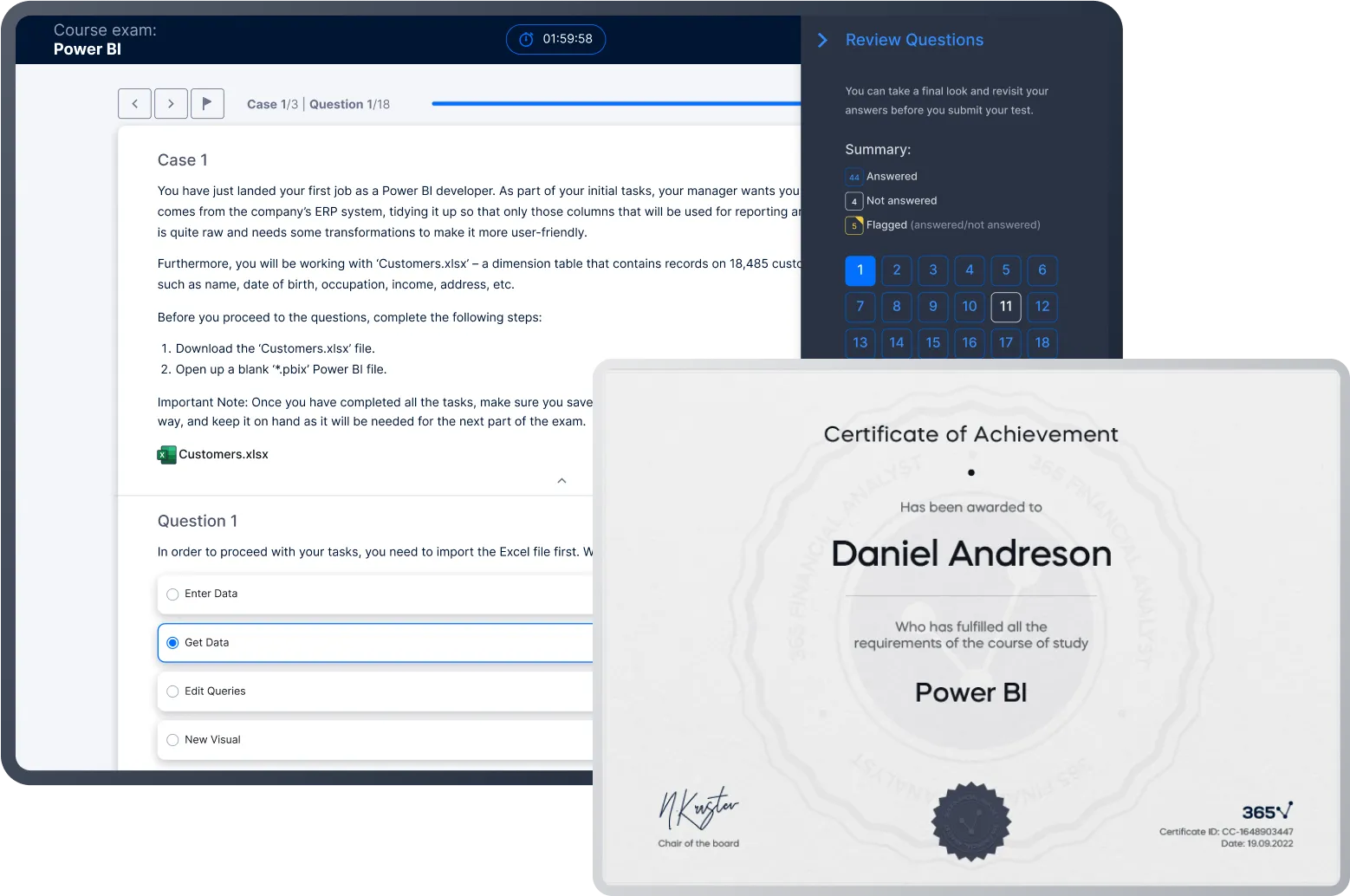

- Course exam

- Certificate of achievement

Advanced Machine Learning and AI Applications in Finance

Start for free

What you get:

- 3 hours of content

- 2 Interactive exercises

- 8 Coding exercises

- 46 Downloadable resources

- World-class instructor

- Closed captions

- Q&A support

- Future course updates

- Course exam

- Certificate of achievement

Start for free

What you get:

- 3 hours of content

- 2 Interactive exercises

- 8 Coding exercises

- 46 Downloadable resources

- World-class instructor

- Closed captions

- Q&A support

- Future course updates

- Course exam

- Certificate of achievement

What you learn

- How to apply advanced machine learning methods

- Techniques for handling the unique challenges of financial data

- Practical feature engineering for market data

- How to use machine learning in portfolio optimisation

- Cutting-edge applications of AI in asset pricing and portfolio management

Top Choice of Leading Companies Worldwide

Industry leaders and professionals globally rely on this top-rated course to enhance their skills.

Course Description

This course teaches you how to apply advanced machine learning and AI techniques to real-world financial problems. Through hands-on projects in Python, you will explore practical applications such as time series forecasting, portfolio optimization, and asset pricing using real financial datasets.

Rather than focusing solely on theory, the course emphasizes implementation and real case studies that mirror the challenges faced by modern financial analysts and quantitative professionals. You will learn how to build, train, and evaluate machine learning models designed for financial data, gaining the skills needed to extract insights and support data-driven investment decisions.

By the end of the course, you will be able to design and implement AI-powered solutions for financial analysis, bridging the gap between advanced machine learning techniques and practical applications in finance.

Section 1 begins with a concise refresher on essential ML concepts, such as the bias-variance trade-off, overfitting, and cross-validation, before showing why standard validation methods often fail in finance.

In Section 2, the focus shifts to predictive modelling for financial time series. You’ll engineer features from raw market data (returns, volatility, lags) using Pandas and yfinance, then explore models ranging from ARIMA and ARIMAX to ensemble methods like Random Forests and Gradient Boosting. You will compare frameworks such as XGBoost, LightGBM, and CatBoost, implement walk-forward validation, and use SHAP values to interpret predictions. Special attention is given to avoiding common pitfalls like look-ahead bias and data leakage with techniques such as purging and embargoing.

Section 3 explores portfolio optimisation and asset pricing. You will apply machine learning to forecast risk and return, building on classic mean-variance optimisation with tools like cvxpy and PyPortfolioOpt. Advanced topics include the Black-Litterman model, shrinkage estimators, Hierarchical Risk Parity, and Eigenportfolios. For asset pricing, you’ll extend traditional factor models with Random Forests and Neural Networks to go beyond the Fama-French framework. We conclude with Reinforcement Learning for dynamic portfolio optimisation, where you will implement an Actor-Critic approach and design reward functions tailored to financial objectives.

By the end of this course, you will have a practical, working knowledge of how to apply machine learning and AI in finance—whether to develop trading strategies, construct portfolios, or build asset pricing models. You will gain not only the technical tools but also the intuition and confidence to use them effectively.

Are you ready to explore the frontier of ML-driven finance? Let’s get started.

Learn for Free

1.1 Getting started

1 min

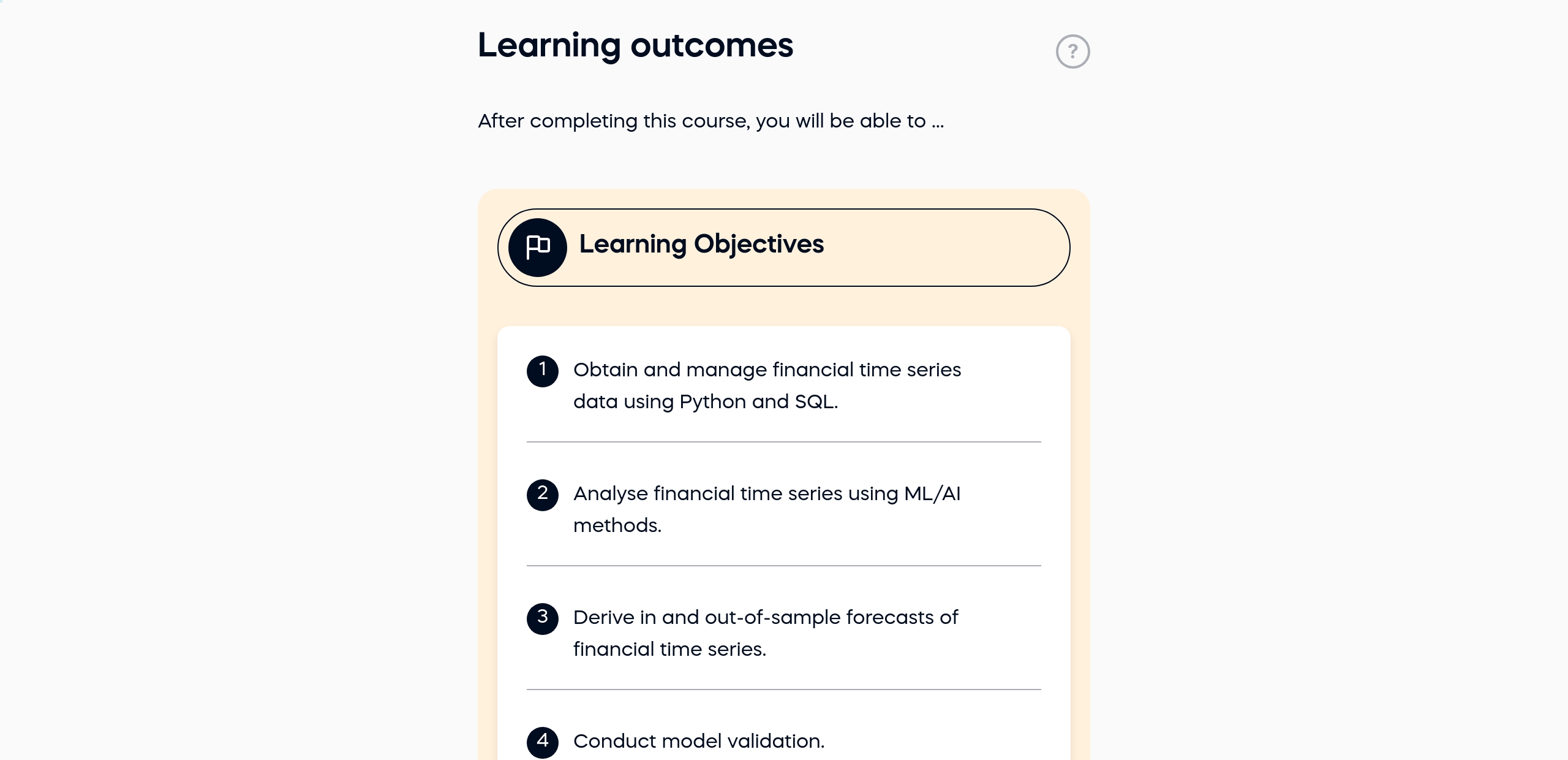

1.3 Learning outcomes

1 min

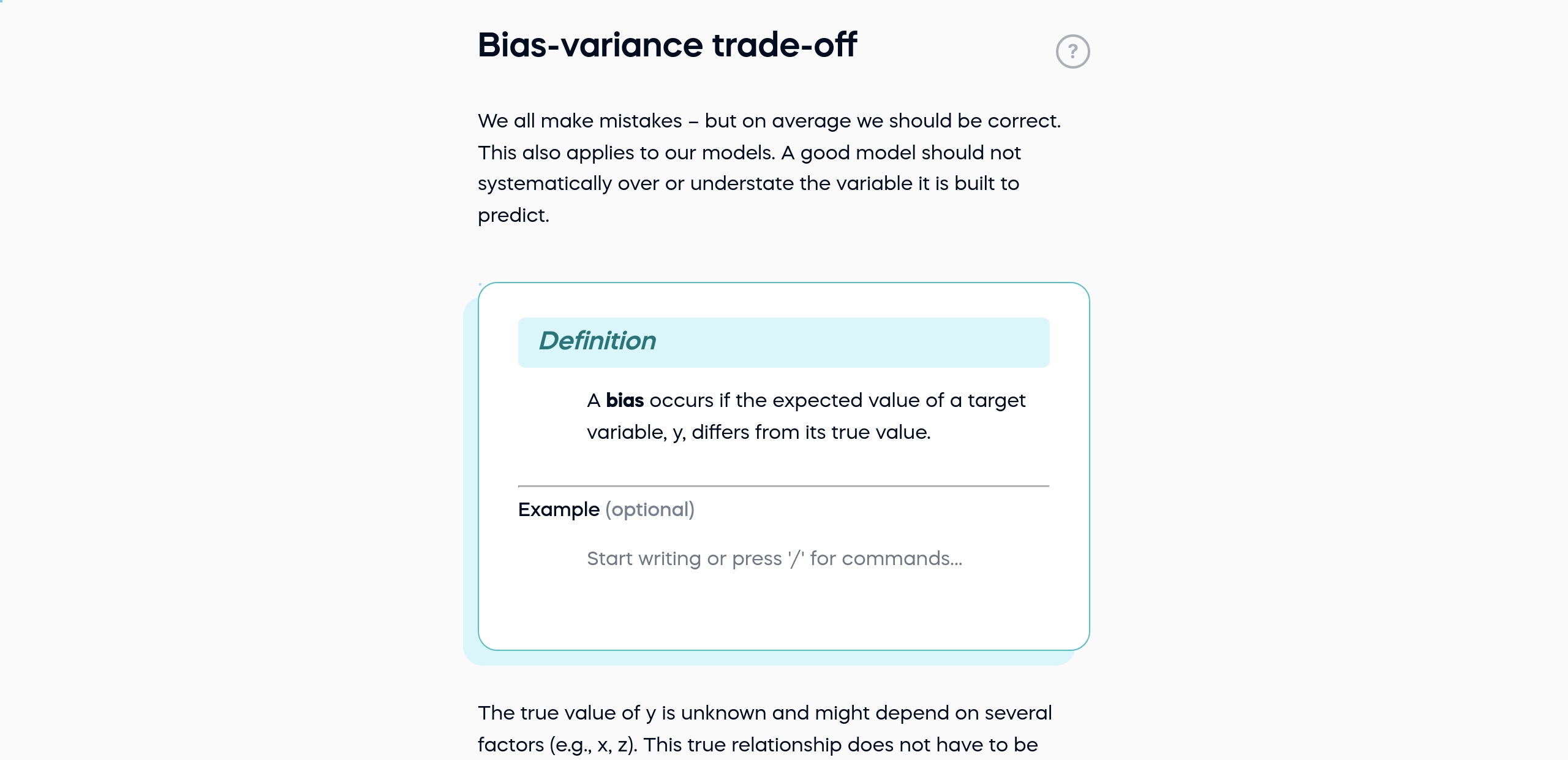

1.5 Bias-variance trade-off

2 min

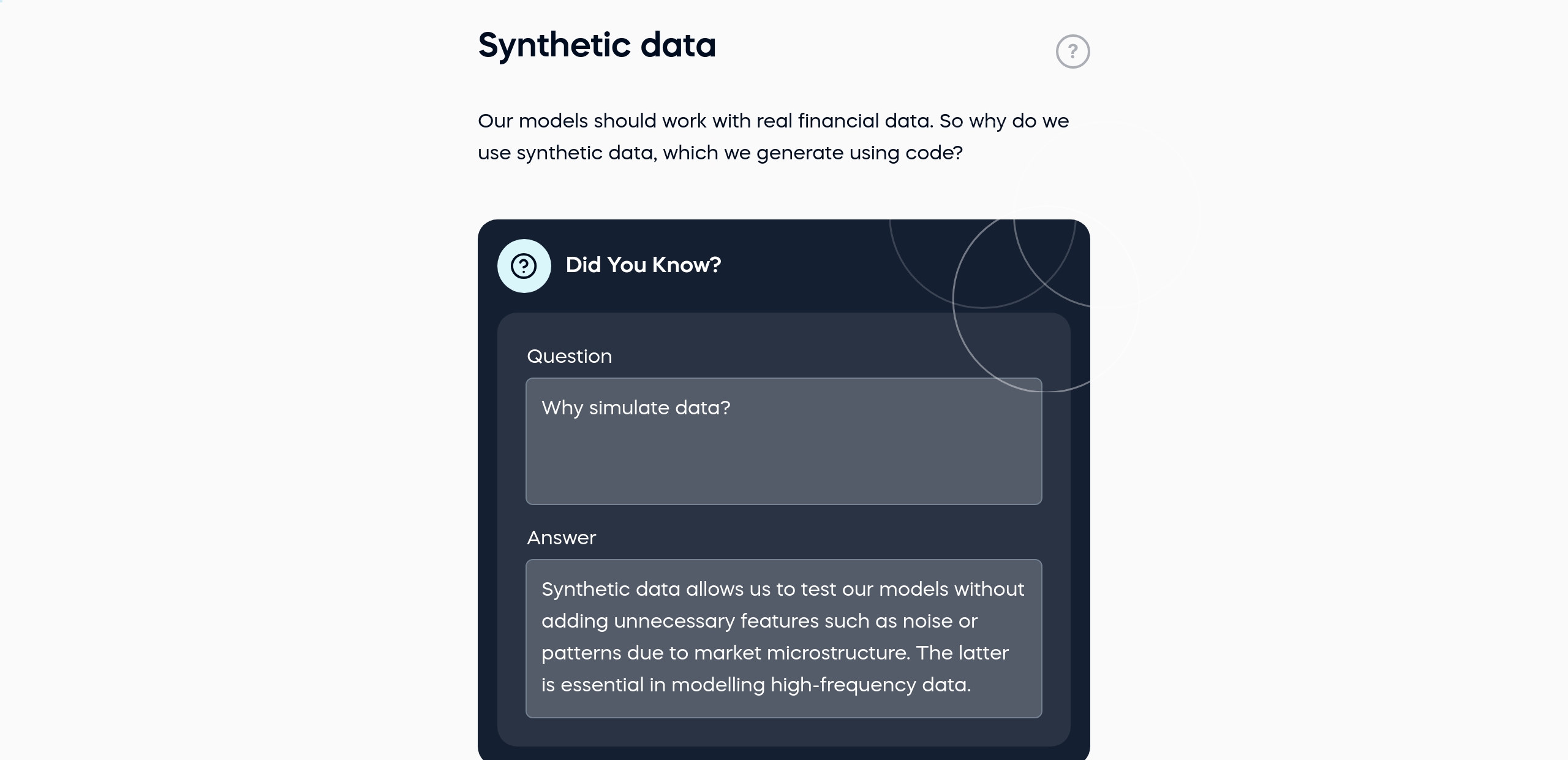

1.7 Synthetic data

1 min

1.8 The bias-variance trade-off in Python

2 min

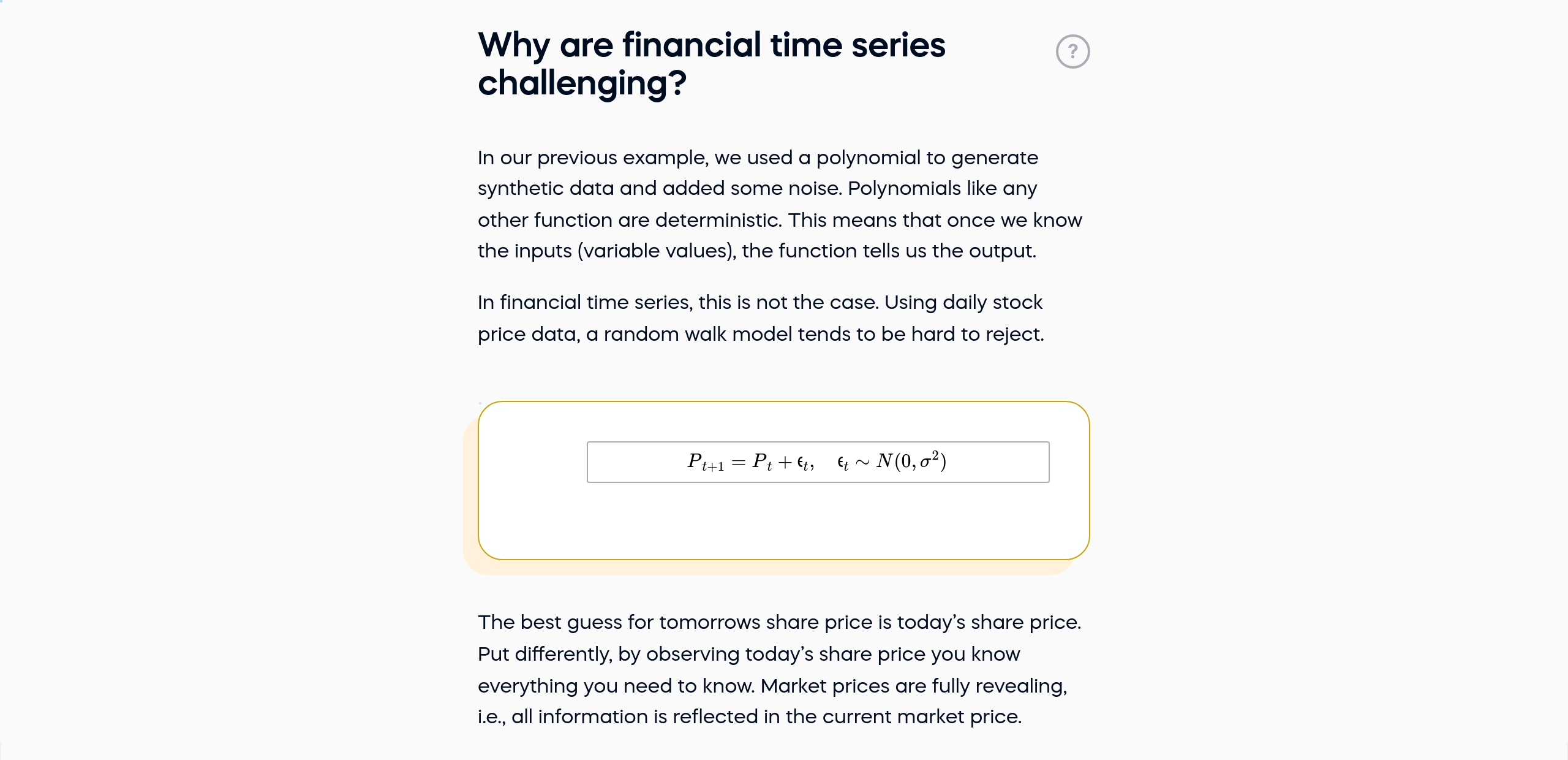

1.10 Why are financial time series challenging?

1 min

Curriculum

- 2. Advanced Predictive Modelling for Financial Time Series22 Lessons 41 Min

We see ML tools in action trying to predict financial time series. Different markets are explored such as stock markets, commodities, cryptos, and interbank markets.

What will you learn? Read now1 minTime series features Read now1 minExploring energy prices4 minFinancial data Read now1 minRefresher: stationarity2 minARIMA models Read now2 minModelling oil prices5 minARIMAX Read now1 minRandom Forests2 minTransformation of time series Read now1 minRandom Forests in Python4 minWhat about non-stationarity? Read now1 minWalk-forward validation Read now1 minSHAP values Read now1 minGradient Boosting Machines2 minGBMs in Python Read now1 minTemporal constraints Read now1 minThe performance–interpretability trade-off2 minXGBoost, LightGBM, and CatBoost Read now1 minComparison of the frameworks5 minModel validation challenges Read now1 minLook-ahead bias and data leakage Read now1 min - 3. ML/AI for Portfolio Management and Asset Pricing21 Lessons 59 Min

Starting with mean-variance optimisation, we explore recent ML/AI applications such as Random Forests and Neural Networks for factor models in asset pricing.

ML for optimal portfolio construction2 minMean-variance revisited Read now1 minML-based risk/return forecasting5 minLimitations of risk-return forecasting Read now1 minBlack-Litterman model Read now2 minPortfolio optimisation using CVXPY3 minPyPortfolioOpt: An alternative package Read now2 minRisk-based portfolios3 minThe Maximum Diversification Portfolio in Python3 minEigenportfolio Read now2 minHierarchical risk parity (HRP)2 minWarnings Read now1 minFama-French extensions using Random Forests8 minOLS, Random Forests or Neural Networks Read now2 minReinforcement learning for portfolio optimisation4 minThe portfolio class5 minThe actor class Read now2 minThe critic class Read now1 minThe training loop5 minModel evaluation in reinforcement learning4 minNext steps1 min

Topics

Course Requirements

- Python (Pandas, NumPy)

- Basic understanding of time series analysis

- Basic understanding of machine learning

Who Should Take This Course?

Level of difficulty: Advanced

- Finance professionals and analysts who want to enhance their forecasting, portfolio management, and asset pricing skills with modern ML and AI tools.

- Data scientists and machine learning practitioners interested in applying their expertise to the financial domain, with its unique data challenges.

- Graduate students and researchers in finance, economics, or quantitative fields looking to build hands-on experience with Python-based financial modelling.

- Aspiring quants and traders who want to develop practical, ML-driven strategies for trading, investment, and risk management.

Exams and Certification

A 365 Financial Analyst Course Certificate is an excellent addition to your LinkedIn profile—demonstrating your expertise and willingness to go the extra mile to accomplish your goals.

Meet Your Instructor

I am a Chair in Finance at the University of Aberdeen with 20 years of experience in higher education, having previously held positions at SOAS, the University of Southampton, UWE, and Utrecht University. As a Practice Specialist in Corporate Finance at McKinsey & Company, I primarily focused on firm valuation and mergers and acquisitions (M&As). Since January 2022, I have served as the Director and Secretary of YUNIKARN LTD, an educational content creation and consulting firm. The company’s YouTube channel, YUNIKARN, offers free courses in data science using Python and Stata. I have provided consulting services for notable organizations, including McKinsey & Company (2007–2010), HMRC (2012–2015), Industrial Bank (China) (2013), Brunello Cucinelli (2018), China State Shipbuilding Corporation (2019), the Third Bureau of Supervision of SASAC (2019), and the Economic Research Institute for ASEAN and East Asia (ERIA) (2021–2022). With a background in economics (PhD, BSc/MSc), mathematics (BSc/MSc), and programming (Python, C/C++, MATLAB, Stata, etc.), I specialize in machine learning (ML), artificial intelligence (AI), and their applications in FinTech. I have acted as principal or co-investigator on several large-scale projects, including initiatives in FinTech (ESRC-NSFC: GBP 0.5 million), IoT (FP7: EUR 2.6 million), and satellite technology (FP6: EUR 11.9 million).

What Our Learners Say

365 Financial Analyst Is Featured at

Our top-rated courses are trusted by business worldwide.